Over the years, I’ve seen property development loans sail through approval — and I’ve seen others fall apart at the final hurdle. More often than not, the difference wasn’t the project itself, but how well the borrower presented their case.

If you’re already looking at land, have development plans on the table, or you’re gearing up to take that next step, this is the stage where confidence matters most. Securing finance is the make-or-break moment for any property development project.

The good news is, you can improve your odds significantly by knowing what lenders look for — and preparing your case properly.

But before you start building your pitch, it’s important to understand two things:

- What category your loan will fall into (residential or commercial).

- What type of lender you’ll be approaching (a bank or a specialist).

Each scenario changes what lenders want to see from you.

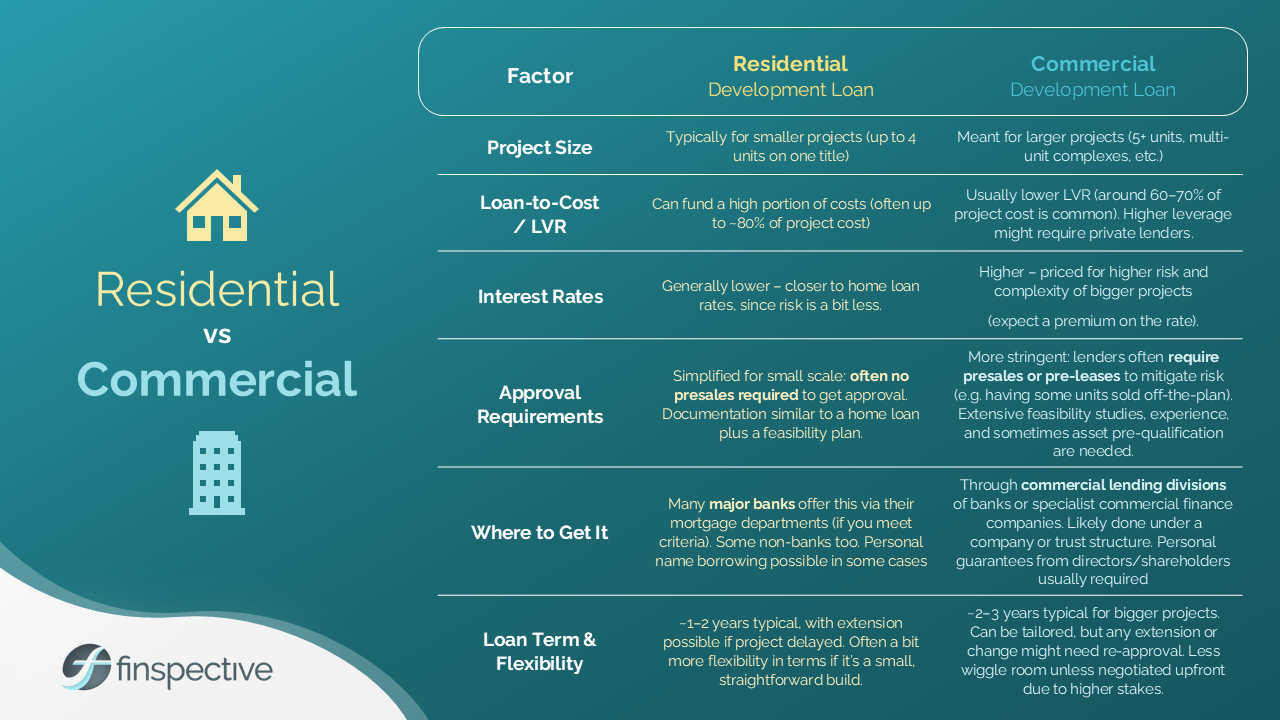

Residential vs Commercial: Where Do You Fit?

One of the first things a lender will do is classify your project. And this classification will shape everything about your approval process.

- Residential development loans usually cover smaller projects — up to four dwellings on a single title. They’re simpler to obtain, with higher loan-to-value ratios (up to ~80%) and fewer requirements around pre-sales. Documentation is closer to what you’d provide for a standard home loan, with the addition of a feasibility plan.

- Commercial development loans apply once you step into larger territory — five or more dwellings, land subdivision or large-scale builds. These loans are assessed much more strictly, with lower loan-to-value ratios (often 60–70%), mandatory pre-sales, and detailed feasibility studies.

I can’t tell you how many times I’ve seen clients surprised when their townhouse build tipped them over into commercial territory. Suddenly, the requirements doubled, and their carefully prepared documents no longer matched what the lender needed.

Approval tip:

- For residential loans, focus on clear but simple documentation, showing the numbers stack up.

- For commercial loans, prepare to prove viability from multiple angles: profit margin, team experience, pre-sales, marketability and contingency planning.

Banks vs Specialist Lenders: Choosing the Right Path

The second decision point is the type of lender you approach. Each has its own appetite for risk, and understanding this upfront helps you tailor your case.

- Banks are conservative. They offer lower interest rates but prefer small, lower-risk projects. Their criteria are strict, and they expect conservative assumptions in your feasibility plan. If you fit neatly within their boxes, banks can be a cost-effective choice.

- Specialist lenders — including private financiers — are more flexible. They’ll fund projects banks won’t touch and can move faster. The trade-off is higher interest rates, but their criteria are often more practical and aligned to real-world development challenges.

I’ve seen clients change their presentation entirely when moving from a bank to a specialist. With the bank, we emphasised stability, conservative forecasts, and risk management. With the specialist, we highlighted opportunity, the project’s market fit, and the strength of the builder. The project didn’t change — but the pitch did.

Approval tip:

- Pitching to a bank? Keep your assumptions conservative and show strong personal financial stability.

- Pitching to a specialist? Demonstrate the project’s potential upside, your team’s experience, how you’ve accounted for risks and why you’re looking at this funding strategy

Building a Strong Case for Your Property Development Loan

Once you know your loan category and lender type, you can focus on the most important part: presenting a strong case. This is where approvals are won or lost. Over the years, I’ve seen five key factors make all the difference.

- A rock-solid feasibility plan

- This is your business case. Break down costs, timelines, and projected sales clearly.

- A profit margin of 15% is the benchmark lenders expect. Anything less, and they’ll question viability.

- Lenders don’t want promises — they want numbers that prove your project stacks up.

- The experience of your team

- Lenders don’t just look at you; they look at your builder, architect, and Engineer and other consultants.

- Even if you’re a first-time developer, a strong team can provide the credibility you need.

- I’ve seen first-time borrowers win approvals purely on the back of their teams proven track record.

- Contingency planning

- No development runs perfectly. Budget for overruns and timeline blowouts.

- Demonstrating foresight here shows professionalism — and makes lenders more comfortable backing you.

- Pre-sales or commitments

- For commercial projects, some form of pre-sales are often non-negotiable. They prove market demand and reduce risk.

- Even for residential projects, showing buyer interest can strengthen your case.

- Evidence of your own financial stability

- A clean credit history, manageable existing debts, and proof that you can handle repayments during construction go a long way.

- Lenders want reassurance that you’re not overextended personally.

When you present these five factors clearly, you shift how lenders see you. Instead of being a risk they have to manage, you become a partner they can trust.

Common Mistakes That Jeopardise Approval

I’ve seen great projects fall apart for reasons that could have been avoided. Some of the biggest missteps are:

- Rushing or submitting incomplete feasibility documents.

- Overestimating profits or underestimating costs.

- Failing to highlight the team’s experience.

- Ignoring contingency planning.

- Pitching the same case to every lender instead of tailoring it.

Too often, borrowers assume the lender will “fill in the blanks.” The truth is, they won’t. If your case isn’t clear and compelling, they’ll simply move on. The frustrating thing is that many of these issues are avoidable. Often, it’s not the project that fails to meet the criteria, but the way it’s presented.

At its core, approval comes down to credibility. When you can demonstrate that your project is viable, that the numbers stack up, and that you’ve assembled the right team, lenders start to see you not as a risk, but as a partner.

If you’ve seen as many Property Development Loans as I have, you’ll have realised that loan approval isn’t about luck. It’s about preparation, planning, and presenting your case in a way that makes lenders confident in your success.

If you’ve got the land or the plans in place, the last thing you want is your finances to be the stumbling block. I’ve seen enough applications succeed — and enough fail — to know what lenders are really looking for. And when you get those fundamentals right, you’ll find the process far less daunting than it first appears.

If you want to keep you one step ahead of the wealth game and on a path towards securing a brighter financial future, check out our page on Investment Loans to find our more

Any advice on this site is general nature only and has not been tailored to your personal objectives, financial situation and needs. Please seek personal advice prior to acting on this information. Any advice on this website has been prepared without taking account of your objectives, financial situation or needs. Because of that, before acting on the advice, you should consider its appropriateness to you, having regard to your objectives, financial situation or needs.